(Zero Hedge)—On Friday the NY Times published a report highlighting the Trump administration’s increasing use of software from data analysis firm Palantir, which has been deployed across at least four federal agencies for the stated purpose of increasing operational efficiency through data modernization.

For now, each deployment of Palantir software is focused on department-specific services, but the fact that they’re now embedded across multiple agencies – combined with Trump’s March executive order calling for the federal government to share data across agencies – has raised concerns over whether the US government is laying the groundwork for what could become an interconnected and unified surveillance apparatus created by a company which has been in business with the government since 2008.

On Wednesday we noted that Fannie Mae, the quasi-government financial firm overseen by the Federal Housing Finance Agency (FHFA), announced a partnership with Palantir to detect mortgage fraud using the firm’s proprietary technology, which includes some elements of artificial intelligence.

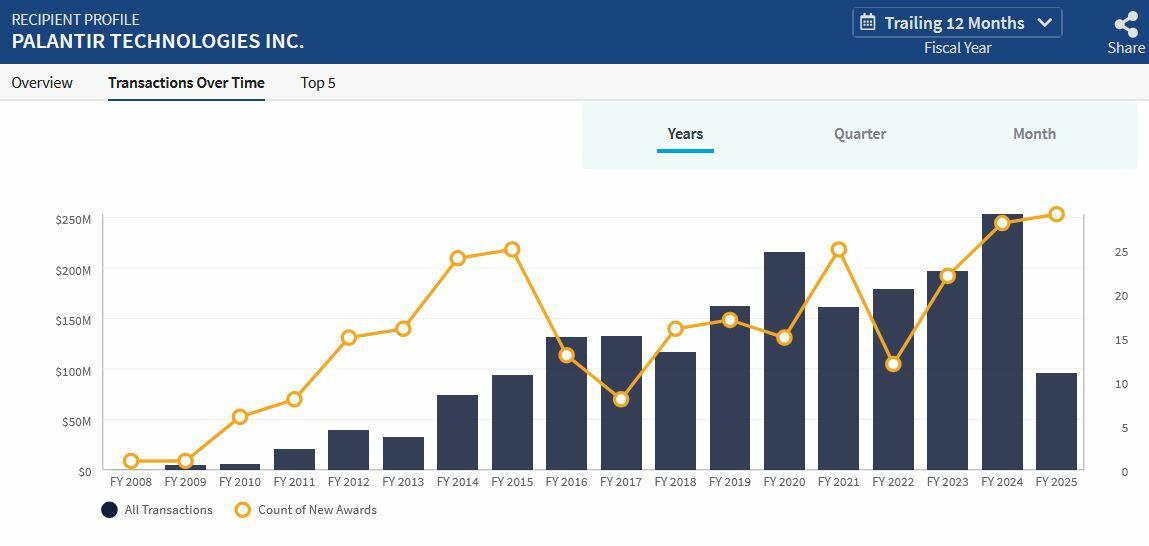

According to the report, since Donald Trump took office Palantir has received over $113 million in government spending – which doesn’t include a $795 million contract from the Department of Defense (DoD) awarded last week. According to the Times report (citing six alleged government officials and Palantir employees), the company is also in discussions with the Social Security Administration and the Internal Revenue Service (the latter of which contracted with Palantir during the Biden administration).

Former Employees Revolt

Palantir was founded in 2003 by Alex Karp and Trump ally Peter Thiel, and specializes in finding patterns in data and streamlining it into easily presentable formats. While Thiel is clearly a conservative, Karp – a self-described “socialist” who voted for Hillary Clinton, bragged about stopping the “far right” in Europe.

CIA agent and head of Palantir Alex Karp says his company’s software “single-handedly” stopped the “far right” in Europe.

Founded in 2003 with funding from the CIA’s In-Q-Tel program, Palantir’s only client before 2008 was the CIA. pic.twitter.com/Shq0uA5x16

— Reed Cooley (@ReedCooley) May 31, 2025

And so it’s of little surprise that employees would flip out and leave over Palantir’s recent $30 million contract with ICE to build a platform to track migrant movements in real time. (Palantir notably designed software for the Israel Defense Forces (IDF) to identify and track Hamas targets).

This month, 13 former employees signed a letter urging Palantir to stop its endeavors with Mr. Trump. Linda Xia, a signee who was a Palantir engineer until last year, said the problem was not with the company’s technology but with how the Trump administration intended to use it.

“Data that is collected for one reason should not be repurposed for other uses,” Ms. Xia said. “Combining all that data, even with the noblest of intentions, significantly increases the risk of misuse.”

…

Ms. Xia said Palantir employees were increasingly worried about reputational damage to the company because of its work with the Trump administration. There is growing debate within the company about its federal contracts, she said.

“Current employees are discussing the implications of their work and raising questions internally,” she said, adding that some employees have left after disagreements over the company’s work with the Trump administration.

Last week, a Palantir strategist, Brianna Katherine Martin, posted on LinkedIn that she was departing the company because of its expanded work with ICE. -NY Times

According to Xia’s letter, “We no longer believe Palantir’s executives are upholding these values. By supporting Trump’s administration,Elon Musk’s DOGE initiative, and dangerous expansions of executive power, they have abandoned their responsibility and are in violation of Palantir’s Code of Conduct.”

“As Musk’s DOGE operation dismantles U.S. government institutions under the guise of exposing corruption, opposition remains silent. Companies are placating Trump’s administration, suppressing dissent, and aligning with his xenophobic, sexist, and oligarchic agenda.Government databases are already erasing references to transgender people and gender-affirming care.These injustices could be facilitated by the very software infrastructure we help build.”

Palantir Responds

In response to the Times, Palantir pointed to a blog post on how the company handles data, which reads: “We act as a data processor, not a data controller.”

“Our software and services are used under direction from the organisations that license our products: these organisations define what can and cannot be done with their data; they control the Palantir accounts in which analysis is conducted.”

What say you?

Safeguarding Your American Dream: Discover the Power of America First Healthcare

In today’s economy, healthcare costs remain one of the biggest threats to financial stability and family security. Americans work hard to build a better life, yet rising medical expenses can quickly erode savings, force tough trade-offs, and even push families toward debt or bankruptcy. Medical bills continue to rank as the leading cause of personal bankruptcy in the United States, with millions facing underinsurance or unexpected out-of-pocket burdens that no one plans for. Many turn to government-run marketplace plans under the Affordable Care Act, hoping for relief, only to discover that what appears affordable on paper often delivers higher long-term costs, limited real protection, and coverage that may not align with personal values or family needs.

America First Healthcare stands out as a private insurance agency dedicated to helping conservatives and families secure better coverage and better rates through customized, values-aligned options. By conducting free insurance reviews, the agency uncovers hidden gaps in existing policies and connects clients with private alternatives that emphasize personal responsibility, small-government principles, and genuine affordability—often delivering up to 20% savings while providing stronger protection for the American Dream.

The allure of marketplace plans is easy to understand: open enrollment periods, premium tax credits for many households, and the promise of “comprehensive” benefits mandated by law. Yet recent data reveals a different reality, especially after the expiration of enhanced premium subsidies at the end of 2025. Enrollment for 2026 dropped by more than one million people compared to the prior year, with many shifting to lower-tier bronze plans to keep monthly premiums manageable.

These plans feature significantly higher deductibles—averaging around $7,500 nationally—and greater cost-sharing requirements. Families who once paid modest amounts after subsidies now face average premium increases of $65 or more per month, even as they accept plans that leave them responsible for thousands in upfront costs before meaningful coverage kicks in.

High deductibles create a dangerous barrier to care. Studies show that people in such plans are less likely to seek timely treatment for chronic conditions, attend preventive screenings, or fill necessary prescriptions. A seemingly minor illness or injury can balloon into major expenses when patients delay care until problems worsen. For a family of four, a single hospitalization, cancer diagnosis, or unexpected surgery can easily exceed the deductible, triggering coinsurance and out-of-pocket maximums that still leave substantial bills. One recent analysis noted that some proposed changes could push family deductibles toward $31,000 in future years, further exposing households to financial risk.

Beyond the numbers, marketplace plans often carry structural limitations. Coverage for certain critical services may include waiting periods or narrower networks that restrict access to preferred doctors and specialists. Preventive care is required to be covered without cost-sharing, but everything else—lab work, imaging, specialist visits, or ongoing treatment—typically waits until the deductible is met. This reactive model contrasts sharply with the proactive, holistic approach many families prefer, especially those focused on wellness, early intervention, and maintaining health to enjoy life rather than merely reacting to illness.

Values alignment represents another growing concern. Government-influenced plans operate within a framework shaped by federal mandates and political priorities that may not reflect conservative principles of limited government, personal freedom, and ethical stewardship. Families who want to direct their healthcare dollars toward providers and benefits that honor traditional values sometimes find marketplace options feel misaligned, forcing a compromise between affordability and conviction.

Private alternatives, by contrast, offer year-round flexibility without the restrictions of open enrollment windows. Independent agents can shop across a wider range of carriers to design plans tailored to specific family needs—whether that means lower deductibles for frequent medical users, broader provider networks, or add-ons that support wellness and preventive services from day one. Clients frequently report more stable premiums that do not automatically escalate each year, along with genuine cost savings once the full picture of deductibles, copays, and coverage depth is considered.

Take the experience of real families who made the switch. Amanda C. shared that her new plan felt “way better” than what she had through the marketplace. Johnny Y. noted his previous coverage kept increasing annually until he found a more stable private option. Sofia S. expressed delight with her plan and began recommending it to others. These stories echo a common theme: when families move beyond one-size-fits-all government marketplaces, they often discover customized protection that better safeguards both health and finances.

Founder Jordan Sarmiento’s own journey underscores the stakes. In 2021, a six-day hospitalization generated a $95,000 bill. Under a well-structured private “Conservative Care Coverage” plan, his out-of-pocket responsibility would have been just $500. That stark difference illustrates how thoughtful planning and private options can prevent a medical event from becoming a financial catastrophe.

Practical steps exist for anyone questioning their current coverage. Start with a no-obligation review of your existing policy to identify gaps—high deductibles, limited critical-care benefits, or escalating premiums. Compare total projected costs (premiums plus potential out-of-pocket expenses) rather than monthly premiums alone. Consider family health history, anticipated needs, and lifestyle priorities. Private agencies can present side-by-side options that include stronger wellness incentives, broader access, and plans built on shared values of self-reliance and freedom.

In an era when healthcare inflation continues to outpace general cost-of-living increases, relying solely on marketplace solutions carries growing risk. Families who proactively explore private alternatives frequently achieve meaningful savings while gaining peace of mind that their coverage truly works when needed most.

America First Healthcare makes this exploration straightforward through its free review process. Families and individuals receive personalized guidance to close coverage holes, reduce unnecessary expenses, and secure plans that align with conservative principles—protecting wallets, health, and the American Dream without government overreach. Many who complete a review discover they can enjoy better benefits for less, often saving up to 20% while gaining the customization and stability that marketplace plans struggle to deliver.

Ultimately, protecting your family’s future requires looking beyond the marketing of “affordable” government options. By understanding the long-term costs hidden in high deductibles, shifting coverage tiers, and values mismatches, Americans can make empowered choices. Private, values-driven insurance offers a smarter path—one that rewards diligence, supports wellness, and delivers real security. For those ready to move beyond the limitations of traditional marketplace plans, a simple review can reveal options designed to serve families, not bureaucracies. The American Dream thrives when individuals and families retain control over their healthcare decisions, and thoughtful private coverage plays a vital role in making that possible.

{kind=link}