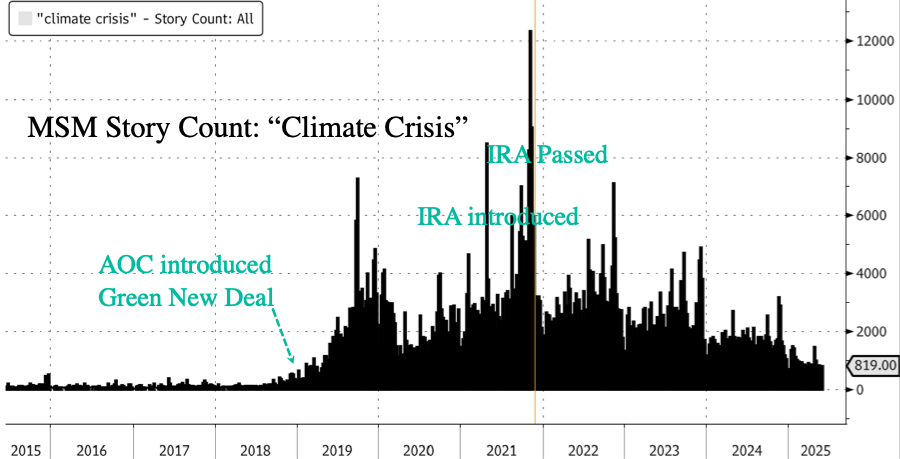

(Zero Hedge)—It’s no secret that progressive billionaire elites, their dark money-funded NGOs, far-left lawmakers, and legacy corporate media orchestrated one of the most elaborate propaganda campaigns in recent memory—weaponizing the narrative of an imminent “climate crisis” to ram through green legislation on Capitol Hill. The result? A massive heist on the Treasury, all under the noble guise of saving the planet.

It’s almost as if the “climate crisis” only dominated headlines when Democrats needed political cover to push green legislation through Capitol Hill…

Now, the darker side of the green scam is coming into focus. Reuters reported earlier this week that a draft tax bill released by Senate Finance Committee Chair Mike Crapo (R-Idaho) proposes an accelerated phaseout of clean energy subsidies established under the Biden-Harris regime’s 2022 Inflation Reduction Act. Specifically, the legislation would significantly dial back solar and wind tax credits to 60% of their original value starting in 2026, with complete elimination by 2028. Under current law, these credits are scheduled to begin phasing out in 2032, meaning the proposal would effectively shorten the incentive window.

Crapo stated in a press release that this draft bill “achieves significant savings by slashing Green New Deal spending and targeting waste, fraud and abuse in spending programs while preserving and protecting them for the most vulnerable.”

Slashing clean energy tax credits, essentially the lifeline of the green industry, would unleash a tsunami of bankruptcies across the sector. Think of Solyndra’s high-profile collapse under the Obama administration in 2011—but multiplied many times over.

“It’s not final, but it looks very negative,” said Carter Atlamazoglou, managing director at FTI Consulting, who specializes in renewable energy, referring to the Senate’s latest draft of the tax bill.

Atlamazoglou told the Financial Times, “You’re dealing with a lot of major uncertainty, which makes anyone considering residential solar—from homeowners to financiers—basically wait and see what happens next.”

“Firms are under liquidity pressure and we’re seeing real distress in the industry,” he warned, pointing out that “Things are coming to a head.”

FT cited bankruptcy data showing a sharp uptick in clean energy company failures—starting in 2022 and accelerating significantly by 2024. Many of these firms, heavily reliant on federal tax credits, are now collapsing as subsidies dry up.

Mass liquidations and layoffs are set to plague the industry this year. This trend will be accelerated if those tax credits are eliminated.

“There’s going to be a 50 to 60 per cent downturn in demand. That will wreak havoc on a lot of these solar companies,” warned Ara Agopian, CEO of Solar Insure.

Agopian said, “Many of them will shut their doors as they can’t stay in business without the tax credit.”

Since the release of the Senate draft, solar stocks have crashed: Sunrun is down 36%, SolarEdge is down 30%, Enphase is down 21%, and First Solar is down 19%.

Solyndra’s downfall remains a cautionary tale in the clean energy space…

“We’re looking at a six-month cliff and thousands of businesses having to completely remake their business models in the space of mere months,” CEO Dan Conant of Solar Holler, warned, “It’s just impossible to do.”

Discover the Freedom of True American Healthcare: Why America First is Revolutionizing Protection for Patriots

In a world where government overreach and skyrocketing premiums are squeezing the life out of hardworking Americans, one innovative agency is standing tall for liberty and affordability. Meet America First Healthcare—the private health insurance powerhouse dedicated to putting *you* first.

Founded by entrepreneur Jordan Sarmiento, this isn’t just insurance; it’s a shield for your family’s future, built on the unshakeable belief that private enterprise delivers better results than bureaucratic red tape.

Picture this: Jordan’s own story hits close to home for so many of us. A sudden medical emergency landed him with a staggering $95,000 bill. Under a traditional plan? He’d be buried in debt. But with America First’s patented health insurance, that nightmare shrank to just $500 out-of-pocket. That’s not a fluke—it’s the promise of coverage that works *for you*, from day one.

Breaking Free from the Chains of Conventional Coverage

Let’s face it: The status quo stinks. Marketplace.gov and big-insurance behemoths hit you with sky-high deductibles—thousands you’d have to pay before benefits even kick in—leaving massive holes in your protection. Need a routine mammogram, colonoscopy, or EKG? Good luck without forking over more cash. And don’t get us started on the gaps in dental, vision, or critical illness support when heart attacks, cancer, or kidney failure strike.

America First Healthcare flips the script. As a proud advocate for private solutions over government intervention, they craft custom plans that slash costs by 20% compared to traditional options. We’re talking comprehensive coverage that includes:

- Preventative and Wellness Care: Physical exams, screenings, and EKGs covered right away—no waiting games.

- Telemedicine Access: Virtual doctor visits anytime, anywhere, for that peace of mind.

- Accident and Critical Illness Protection: Real safeguards against life’s curveballs.

- Add-On Boosts: Dental, vision, disability, and supplemental plans to plug every leak.

Whether you’re an individual stepping off your parents’ plan, a growing family with kids in tow, or a small business owner tired of employee headaches, their tailored approach fits like a glove. Small businesses? Unlock group benefit rates usually reserved for corporate giants—without the red tape.

And for those in-between moments? Short-term insurance steps in as an ultra-affordable bridge, while life insurance ensures your loved ones are never left vulnerable.

Real Americans, Real Wins

Don’t just take our word for it. Thousands of freedom-loving families have already ditched the old system for America First. “Finally, insurance that aligns with our values and actually saves us money,” shares one client. Another raves, “Our small team got big-business perks without the hassle—it’s a game-changer.” These aren’t scripted lines; they’re the voices of patriots who’ve reclaimed control over their health destiny.

Your Move: Secure Your Shield Today

Why settle for less when you can demand better? America First Healthcare isn’t about profits—it’s about powering the American dream with reliable, value-driven protection. Plans are available year-round, no open-enrollment nonsense.

Ready to uncover the gaps in your current setup and lock in savings? Schedule your FREE healthcare review today at America First Healthcare. In under 15 minutes, their experts will map out options that fit your life, your budget, and your principles.

America First isn’t just healthcare—it’s a declaration of independence. Join the movement. Your family’s freedom starts now.

{kind=link}