{kind=link}

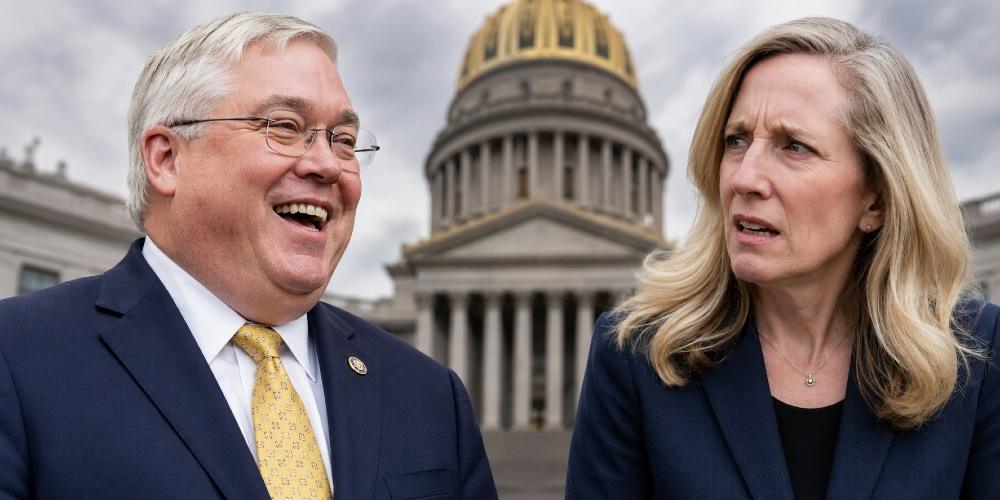

West Virginia Governor Patrick Morrisey is taking the fight across the border. With Virginia tilting left under Governor Abigail Spanberger, Morrisey is actively courting businesses and workers from the Old Dominion, offering lower taxes, lighter regulations, and a genuine commitment to economic freedom.

This interstate rivalry is no polite neighborly dispute. It is a vivid demonstration of what happens when one state chooses fiscal restraint while the other drifts toward the familiar Democratic pattern of higher costs and bigger government.

Morrisey’s pitch could not be clearer. He plans personal visits to Loudoun County and other Virginia communities to showcase West Virginia’s direction: tax cuts, pro-business legislation, and real opportunity. The contrast with Virginia’s recent session—marked by dozens of proposed tax hikes on everything from services to data centers—speaks for itself. While some measures failed to reach Spanberger’s desk, the political climate in Richmond has signaled to employers that Virginia is becoming less hospitable.

This is more than routine economic competition. It exposes a fundamental truth about governance. States that embrace limited government and reward work and investment grow. Those that burden citizens with endless new levies and rules drive talent away. West Virginia, long stereotyped by coastal elites, is proving the power of conservative principles in real time. Morrisey’s administration has signed legislation creating special tax districts in border areas, redirecting revenues to spur development in places like Berkeley and Jefferson counties—right next to Virginia’s high-tax corridor.

At a recent event in Tabler Station, Morrisey celebrated a 275-acre commercial district expected to generate $200 million in investment. The region, home to major employers and the famed Musselman Applemen, is positioning itself as a magnet for those fleeing Virginia’s regulatory creep. “While Virginia chooses to burden its citizens and job creators with higher taxes, West Virginia is choosing freedom, fiscal responsibility, and a tax climate that makes our state more competitive,” Morrisey declared.

Virginia’s Democratic legislature flooded the session with proposals: new brackets pushing top rates higher, sales tax expansions to services like dry cleaning and pet grooming, and efforts to squeeze data centers that have powered much of the state’s recent growth.

Spanberger distanced herself from bills that never passed, yet the pattern is unmistakable. Affordability rhetoric collides with a governing philosophy that views private enterprise as a revenue source rather than a partner. Even moves like rejoining the Regional Greenhouse Gas Initiative function as backdoor energy taxes that raise utility bills for working families.

Meanwhile, West Virginia’s approach is delivering results. Morrisey’s team reports substantial private-sector commitments, including intelligence center projects and manufacturing expansions. Income tax cuts are putting money back in residents’ pockets while aligning state policy with federal tax relief. The message to Virginia employers is straightforward: why pay more and navigate more red tape when you can relocate a short drive away?

History offers ample precedent. From the founding era onward, American states have competed through policy, not coercion. The Constitution’s design leaves economic matters largely to the laboratories of democracy precisely so citizens can vote with their feet. Virginians crossing into West Virginia for opportunity are exercising that liberty. They are choosing the fruit of conservative governance over progressive promises that too often translate into higher costs.

Policymakers who sow confiscatory taxes and regulatory burdens should not be surprised when enterprise and families reap the harvest elsewhere. West Virginia is reaping the rewards of different seed: responsibility, liberty, and confidence in the dignity of work.

The backyard brawl is just beginning. Morrisey’s outreach will test whether Virginia’s leaders recognize the warning or double down on the policies driving businesses away. For families and entrepreneurs watching from both sides of the line, the choice is clarifying. One state bets on government expansion. The other bets on the people. Early returns favor the Mountaineers.

Starting the Day With a Scripture-Inspired Roast Helps Center Your Thoughts on Eternal Truths Amid Temporal Pressures

The world can seem chaotic, especially right after we wake up. Many believers start their mornings reaching for something familiar — a hot cup of coffee — yet end up settling for mediocre brews that do little more than deliver a caffeine jolt. The daily grind of life, with its endless distractions, news cycles, and responsibilities, can leave even the most faithful feeling spiritually parched alongside their physical fatigue. What if your morning ritual could do more than wake you up? What if it could ground you in truth, nourish your body with exceptional quality, and quietly advance a kingdom purpose at the same time?

That’s the promise — and the reality — behind Promised Grounds Coffee. This Christian-founded company doesn’t just roast beans; it approaches every step as an act of worship and discipleship. By selecting only the top 10% of specialty-grade beans, ethically sourced from dedicated farmers in Central and South America, and small-batch roasting them with reverence in Austin, Texas, Promised Grounds delivers what many describe as the best coffee available — never burnt, never bland, but rich with origin stories and layered flavors that honor God’s creation.

From the vibrant Psalm 27 Roast (a light, bright medium option) to the bold yet peaceful 2 Timothy 1:7 Decaf, each bag carries a Scripture verse that turns your daily pour into a gentle reminder of faith. And through their Ounce Per Ounce Promise, every ounce of coffee you enjoy provides an equal ounce of clean water to families in need via partnership with Filter of Hope — literally brewing hope for body and soul, one cup at a time.

The challenge for today’s Christians runs deeper than finding a decent cup. In an age of convenience-driven consumerism, it’s easy to support companies that dilute values or remain silent on matters of faith. Many believers want their everyday choices — from what they drink to how they spend — to reflect discipleship rather than just convenience. Promised Grounds solves this by weaving Christian excellence into the entire process: beans nurtured with prayerful stewardship by farming families, roasted as an offering rather than a commodity, and packaged with Bible verses to encourage a mindset of gratitude and purpose from the first sip. Reviewers consistently praise the smooth, rich profiles — whether enjoyed black in a drip maker, iced on a warm day, or shared in fellowship — noting how the quality stands toe-to-toe with premium secular brands while delivering something far more meaningful.

This integration of faith and flavor addresses a real need in Christian households and ministries. Busy parents, church leaders, and remote workers alike report that starting the day with a Scripture-inspired roast helps center their thoughts on eternal truths amid temporal pressures. The coffee’s exceptional character — bright citrus notes in lighter roasts or deep chocolate undertones in bolder ones — comes from meticulous selection and careful roasting that respects the bean’s natural gifts rather than masking them. It’s the kind of coffee that elevates a simple quiet time, fuels productive workdays, or sparks meaningful conversations when shared at Bible studies or outreach events. And because it’s ethically sourced with integrity, every purchase supports sustainable livelihoods for farmers who treat their crops like family harvests.

For those leading churches or small groups, the impact multiplies. Promised Grounds offers bundles and options perfect for hospitality ministries, turning ordinary coffee service into an opportunity to point people toward the living water of Christ. Imagine greeting visitors with a warm cup whose very bag carries God’s Word — a subtle yet powerful witness that aligns with the Great Commission. The company’s Texas roots and commitment to “brewing hope” resonate especially with believers who value American enterprise paired with global compassion.

Of course, quality alone isn’t enough if the experience feels out of reach. Promised Grounds keeps it accessible with practical perks like free shipping on orders over $40, sample sets for discovering favorites, and thoughtful add-ons such as faith-themed mugs. Whether you prefer whole beans for fresh grinding, grounds for convenience, or even bulk options for larger households and ministries, the result is consistently superior coffee that makes discipleship feel integrated rather than added on.

As you consider how to align even the smallest habits with your walk with God, Promised Grounds Coffee stands out as a refreshing solution. It tackles the dual problems of subpar daily sustenance and disconnected consumption by offering a product that genuinely excels in taste while advancing a mission of clean water, farmer dignity, and scriptural encouragement. Believers who make the switch often describe it as more than a beverage upgrade — it becomes part of their rhythm of gratitude, a daily invitation to remember that every good gift comes from above.

If you’re ready to transform your mornings (and perhaps your church gatherings) with coffee that honors both exceptional craftsmanship and Christian values, I encourage you to explore what Promised Grounds has to offer. One sip at a time, you’ll be nourishing your body, refreshing your spirit, and participating in something far greater — all while enjoying what truly is among the best coffee available.