(Zero Hedge)—The world’s biggest energy execs are currently at the annual CERAWeek conclave in Houston where, understandably, they are dropping bulletin bombs reeking of fire and brimstone, and warning the already critical oil/gas situation will only get worse if the pre-war status quo isn’t restored (which incidentally will be great for their bottom lines… until the world is tipped into a recession).

Take US oil giant Chevron, which warned that California is careening toward an energy crisis because of the Iran war (which will likely be resolved soon), and that the company may quit refining oil in the state unless officials roll back taxes and regulations (which is unlikely to ever be resolved as long as Dems are in charge of the Golden State).

California is highly exposed to the disruption rippling across commodity markets because it imports about 20% of its refined fuels from Asia. But as extensively discussed here, oil product shipments from China, South Korea, Singapore and elsewhere are at risk of slowing significantly as Iran blocks the Strait of Hormuz, leaving Asian nations struggling to meet their own demand at home let alone export to California.

Chevron’s oil refining head Andy Walz said the potential for fuel shortages in California is his worst fear: “We have refineries in Asia that are having to cut crude, and so they’re going to make less products,” Walz said in an interview Tuesday. “What if San Francisco doesn’t have the jet fuel it needs? Or Los Angeles? Or maybe gasoline?”

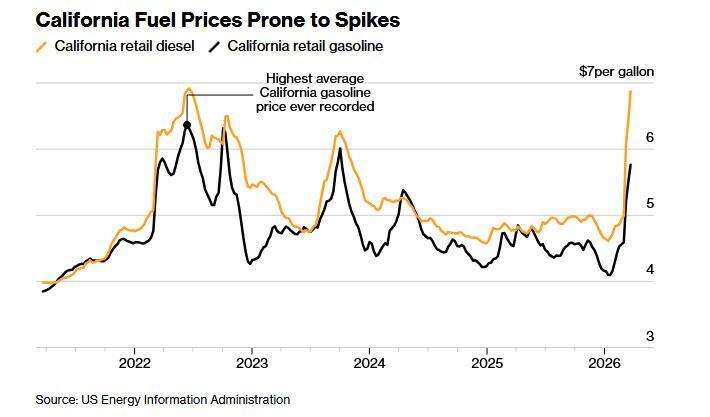

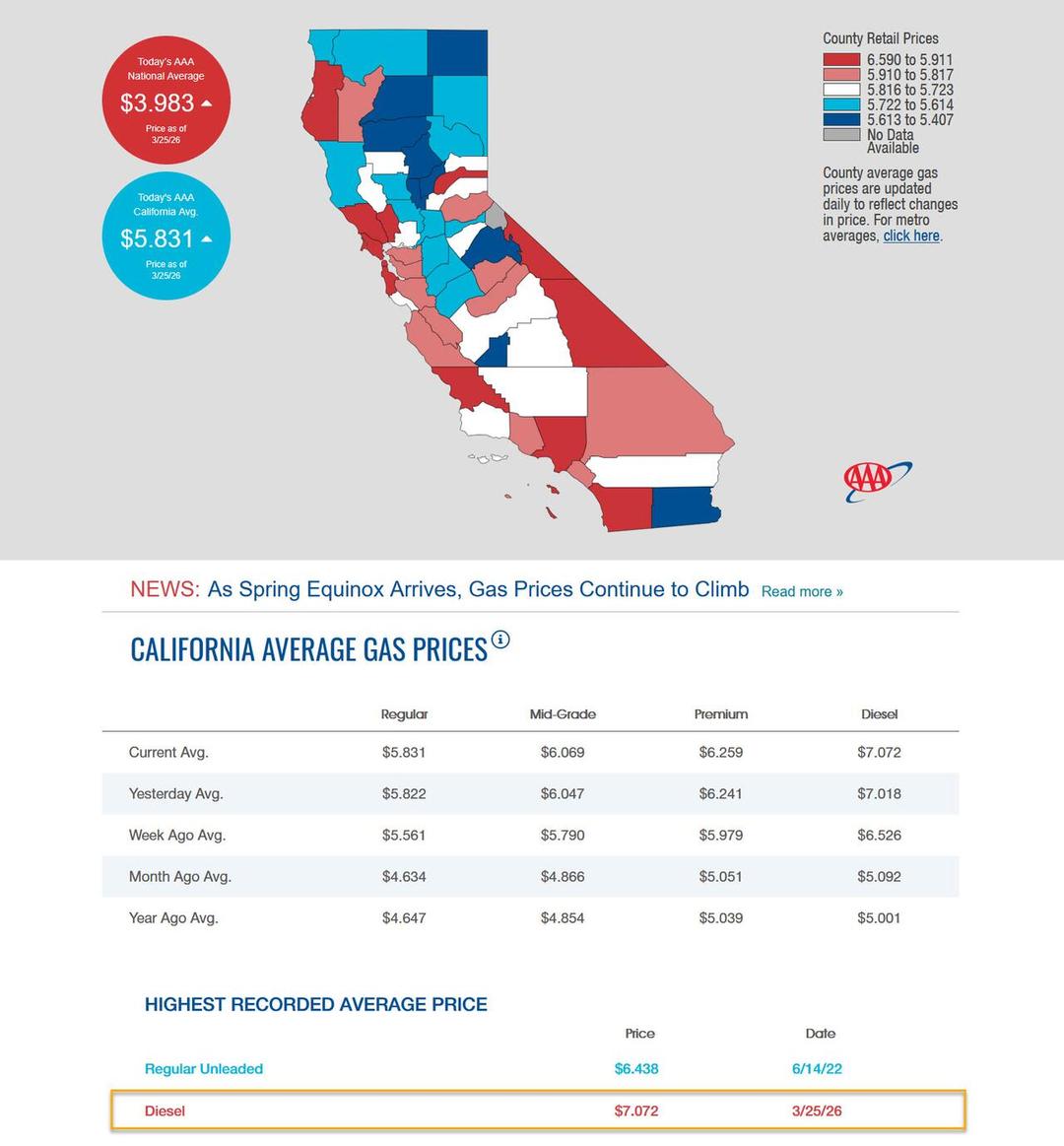

And as if to confirm his warning, just hours later the price of California Diesel hit a record high just above $7 per gallon, or $7.072 to be precise.

That topped the previous record of $7.012 in June 2022, in the first months of Russia’s war in Ukraine.

Since California is disconnected from the US fuel-making centers of Texas and Louisiana, it is essentially an energy island. That’s compounded by multiple refinery closures in recent years due to increased costs driven by regulations designed to fight climate change and cap oil industry profits, not to mention the state’s toxic and oppressive regulatory regime.

As a result, California consumers are more exposed than most other Americans to surging energy prices because of the Iran war. They already pay nearly $6 for a gallon of gasoline, compared with a national average of close to $4, due to the state’s ruinous legacy “green” regime. It’s a growing political problem for Governor Gavin Newsom, a Democrat who is expected to run for president in 2028.

“California has decided that they’re going to rely on imports,” Walz said at the CERAWeek by S&P Global conference in Houston. “It’s a dangerous game”, Walz added tongue-in-cheek.

California officials should declare an “energy emergency,” reform its climate and tax rules and promote in-state oil production, Walz said. Without such action, Chevron could quit refining in California within a decade, he said.

A spokesman for California Governor Newsom’s office said oil companies are “cashing in” on the war in Iran and running a “coordinated campaign” to attack California. In other words nothing will change until prices get to be so high, the state’s residents demand change.

“If they’re serious about protecting consumers, they should direct that concern where it belongs: at Donald Trump. There’s no end in sight to Trump’s war taxing American families at the pump,” the spokesman, Anthony Martinez, said in an email, confirming Newsom’s plan is… to pretend there is no problem.

Meanwhile, anyone with a brain can see what’s coming: the problem in California is one of the state’s own making, Walz said.

The Trump administration has already used emergency wartime powers to authorize Sable Offshore, a Houston-based driller, to restart oil production off the California coast. The president has also temporarily waived a century-old maritime law called the Jones Act to help make it cheaper and easier to ship gasoline, diesel and other commodities between US ports.

Meanwhile, California already has the nation’s toughest fuel standards as well as a carbon cap-and-trade program that critics say forces consumers to pay the highest prices in the nation. Its goal to reduce carbon emissions 85% by 2045 relies heavily on a near-complete phaseout of gasoline-powered cars and a large reduction in heavy industry — including refining.

Nonetheless, California remains the country’s second-largest consumer of gasoline and the largest market for jet fuel, for which there’s currently no practical low-carbon alternative. The Democratic state’s recent revulsion toward Elon Musk, and Tesla, has not helped the looming fuel crisis.

“The California intent to offshore carbon to other nations has offshored their security of supply,” Walz said. “They’ve offshored jobs and they haven’t had any impact on carbon.”

Chevron, which has tankers sitting idle on each side of the Strait of Hormuz, is taking the unusual step of shipping Gulf Coast oil to California through the Panama Canal as the war disrupts shipments from the region that West Coast refiners typically use, Walz said.

China has already imposed a fuel export ban as shipments from the Gulf dwindle. If the Strait of Hormuz remains blocked long enough, other Asian countries could follow suit. Chevron’s scenario planning initially looked at the Strait being closed until the end of March.

“Now our scenario plans are worse,” Walz said. “It’s going to be longer and we’re trying to look around the corner.”

California is home to more than 30 military bases. That includes one of the largest in the US, Travis Air Force Base, which Chevron supplies from its Richmond refinery.

“I think the US government should be concerned,” Walz said.

But wait, there’s more because the state’s green lunatics threaten to make an already dire crisis something truly historic: new emissions rules proposed by the California Air Resources Board, if implemented, threaten to drive costs for the state’s remaining refineries even higher. Chevron estimates the additional expenses could hit $500 million within five years.

“They need to abandon the tax on refineries or they won’t have any refineries in 10 years,” Walz said. “If it stays that way — Chevron will be gone in 10 years for sure. We won’t be able to make it.”

* * *

But it’s not just California that faces a historic crisis: Europe is about to get crushed as well.

According to Shell CEO Wael Sawan, Europe will soon begin to experience the same kind of disruption to fuel supplies that Asia has faced due to the war in Iran in recent weeks. Sawan said the effects of the conflict continue to ripple out across global fuel markets, first in South Asia, then Southeast Asia and Northeast Asia, and increasingly in Europe as April approaches.

“We are trying to work with governments to just alert them to the various levers they will need to pull, including on the demand side, including what they need to do around storage,” he said Tuesday at the same CERAWeek conference.

Just like California, expect Europe to do nothing besides pointing fingers, until it is too late.

Starting the Day With a Scripture-Inspired Roast Helps Center Your Thoughts on Eternal Truths Amid Temporal Pressures

The world can seem chaotic, especially right after we wake up. Many believers start their mornings reaching for something familiar — a hot cup of coffee — yet end up settling for mediocre brews that do little more than deliver a caffeine jolt. The daily grind of life, with its endless distractions, news cycles, and responsibilities, can leave even the most faithful feeling spiritually parched alongside their physical fatigue. What if your morning ritual could do more than wake you up? What if it could ground you in truth, nourish your body with exceptional quality, and quietly advance a kingdom purpose at the same time?

That’s the promise — and the reality — behind Promised Grounds Coffee. This Christian-founded company doesn’t just roast beans; it approaches every step as an act of worship and discipleship. By selecting only the top 10% of specialty-grade beans, ethically sourced from dedicated farmers in Central and South America, and small-batch roasting them with reverence in Austin, Texas, Promised Grounds delivers what many describe as the best coffee available — never burnt, never bland, but rich with origin stories and layered flavors that honor God’s creation.

From the vibrant Psalm 27 Roast (a light, bright medium option) to the bold yet peaceful 2 Timothy 1:7 Decaf, each bag carries a Scripture verse that turns your daily pour into a gentle reminder of faith. And through their Ounce Per Ounce Promise, every ounce of coffee you enjoy provides an equal ounce of clean water to families in need via partnership with Filter of Hope — literally brewing hope for body and soul, one cup at a time.

The challenge for today’s Christians runs deeper than finding a decent cup. In an age of convenience-driven consumerism, it’s easy to support companies that dilute values or remain silent on matters of faith. Many believers want their everyday choices — from what they drink to how they spend — to reflect discipleship rather than just convenience. Promised Grounds solves this by weaving Christian excellence into the entire process: beans nurtured with prayerful stewardship by farming families, roasted as an offering rather than a commodity, and packaged with Bible verses to encourage a mindset of gratitude and purpose from the first sip. Reviewers consistently praise the smooth, rich profiles — whether enjoyed black in a drip maker, iced on a warm day, or shared in fellowship — noting how the quality stands toe-to-toe with premium secular brands while delivering something far more meaningful.

This integration of faith and flavor addresses a real need in Christian households and ministries. Busy parents, church leaders, and remote workers alike report that starting the day with a Scripture-inspired roast helps center their thoughts on eternal truths amid temporal pressures. The coffee’s exceptional character — bright citrus notes in lighter roasts or deep chocolate undertones in bolder ones — comes from meticulous selection and careful roasting that respects the bean’s natural gifts rather than masking them. It’s the kind of coffee that elevates a simple quiet time, fuels productive workdays, or sparks meaningful conversations when shared at Bible studies or outreach events. And because it’s ethically sourced with integrity, every purchase supports sustainable livelihoods for farmers who treat their crops like family harvests.

For those leading churches or small groups, the impact multiplies. Promised Grounds offers bundles and options perfect for hospitality ministries, turning ordinary coffee service into an opportunity to point people toward the living water of Christ. Imagine greeting visitors with a warm cup whose very bag carries God’s Word — a subtle yet powerful witness that aligns with the Great Commission. The company’s Texas roots and commitment to “brewing hope” resonate especially with believers who value American enterprise paired with global compassion.

Of course, quality alone isn’t enough if the experience feels out of reach. Promised Grounds keeps it accessible with practical perks like free shipping on orders over $40, sample sets for discovering favorites, and thoughtful add-ons such as faith-themed mugs. Whether you prefer whole beans for fresh grinding, grounds for convenience, or even bulk options for larger households and ministries, the result is consistently superior coffee that makes discipleship feel integrated rather than added on.

As you consider how to align even the smallest habits with your walk with God, Promised Grounds Coffee stands out as a refreshing solution. It tackles the dual problems of subpar daily sustenance and disconnected consumption by offering a product that genuinely excels in taste while advancing a mission of clean water, farmer dignity, and scriptural encouragement. Believers who make the switch often describe it as more than a beverage upgrade — it becomes part of their rhythm of gratitude, a daily invitation to remember that every good gift comes from above.

If you’re ready to transform your mornings (and perhaps your church gatherings) with coffee that honors both exceptional craftsmanship and Christian values, I encourage you to explore what Promised Grounds has to offer. One sip at a time, you’ll be nourishing your body, refreshing your spirit, and participating in something far greater — all while enjoying what truly is among the best coffee available.

{kind=link}