(Zero Hedge)—Authored by Matthew Piepenburg via vongreyerz.gold. Is gold calling out a broken global financial system? One Big…Lie?

Earlier this year, I was asked to give my most “heretic” opinion about the global financial system. This was an unusual yet bold question, and after a brief pause, I answered that the entire system was…, well:

“A lie.”

This may seem like a sensational response in an industry sometimes prone to the sensational; however, if we look at stubborn facts, the answer is truer than it is extreme.

When it comes to a financial system rotting from within, the Botox-like beauty of our ballooning S&P and centralized credit market hides an aging and decrepit disease.

That is, policy lies, like Botox, can’t hide reality forever, and the evidence of a fatally debt-sick system hiding financial truths behind forked tongues and euphemistic lingo is literally all around us.

A Long List of Truth-Stretching…

From the very era of my birth, the list of lies is almost comical.

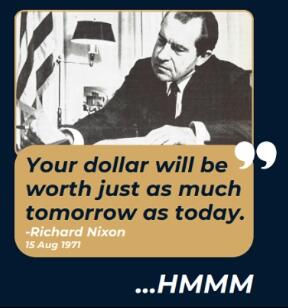

Nixon:

In 1971, for example, when Nixon decoupled the dollar from gold [thereby allowing his own and future administrations the unfettered luxury (and sickness) of expanding (debasing) the money supply], he promised the measure would be “temporary” and that “our dollar would be worth just as much tomorrow as it is today.”

Both statements, of course, were open lies.

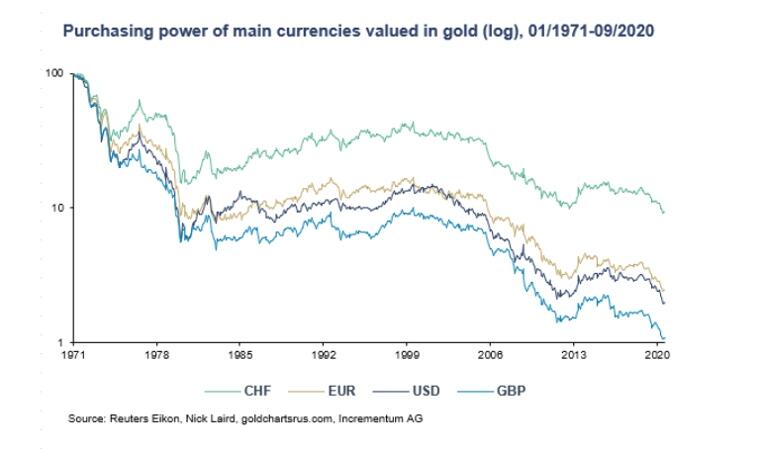

54 years later, the dollar remains un-chaperoned to gold, and when measured against a milligram of that same precious metal, the USD (and other major Fiat currencies) has lost 99% of its purchasing power.

Meanwhile, gold is rising faster against the USD and other world currencies as their purchasing power is diluted by desperate policies to inflate away their debt with debased currencies.

Lying to Our Founding Fathers:

It’s also worth noting that our fiat paper Dollar, un-backed by gold, is a direct contradiction to our Constitution, and in my mind, is itself just another, well…Lie.

Wilson’s Fed:

But long before the lies of 1971, let us not forget the lie of 1913, when Wilson signed an equally unconstitutional Federal Reserve into law, a so-called “independent” bank which is anything but independent (it’s effectively a fourth branch of government) and is neither “Federal” nor a “Reserve.”

Larry Summers:

Fast forward to the great financial crisis of 2008, which was effectively a mortgage—backed-security credit implosion driven by an unregulated derivatives market, and we see even more staggering dishonesty.

A decade before this levered credit implosion, Assistant Treasury Secretary Larry Summers was called to Congress to answer Brooksley Born’s concerns (as head of the CFTC) that these derivative instruments, if left unregulated, would destabilize markets.

Summers publicly embarrassed Born and then told the world that the bankers in charge of these OTC instruments of levered destruction were more than sophisticated enough to manage the risks.

Of course, by the 2008 market implosion, we all knew that assertion was a lie.

Bernanke, Yellen & Powell:

We also know that when the markets tanked in 2008 (thanks largely to Mr. Summers’ deregulation fiasco), Bernanke’s subsequent promise that the money printing which followed (counterfeiting euphemistically called “Quantitative Easing”) would only be a “temporary” measure was just another lie.

QE1 was soon followed by QE 2,3,4 “Operation Twist” and then “Unlimited QE” by 2020.

But such lies are nothing new to central bankers. Remember Yellen?

And let us not forget Powell’s 2021 promise that the inflation (a direct result of the very money printing Bernanke promised would be “temporary” in 2010) facing the USA would only be “transitory.”

We knew then, as we still know today, that transitory inflation, like the very scale which measures CPI, were just more lies.

In fact, lies, like the euphemisms from on top, are almost standard policy from our so-called policy makers.

MMT:

“Modern Monetary Theory,” or “MMT,” for example, is neither modern, nor monetary, nor a theory.

The fantasy of believing a nation can solve a debt crisis via more debt, which is then monetized by creating fake money, has been tried from ancient Rome and 1789 France to 1990’s Yugoslavia.

But as history confirms, it has failed EVERY time.

Other Lies…

Other such lying euphemisms, from the “Patriot Act” and the “Department of Homeland Security” to the “safe and effective” of our now-pardoned “trust the science” leadership may be less economic, but they are no less dishonest—being far more about centralization than anything “patriotic” or “security” driven…

In sum, so many lies, so many examples.

And the fact that 99% of our nation’s now openly distrusted (by greater than 40% of the US population) media outlets are owned by just five mega-corporations, is it any wonder that such lies, as Mark Twain quipped, “can travel half way around the world while the truth is putting on its shoes”?

But as introduced above, eventually the lies can no longer hide what our eyes, intuition, and wallets can see, touch or feel.

Gold: The Ultimate Lie Detector

Toward this end, we clearly know we are reaching an inflection point in the global financial system when even the liars have started to confess the truth, and much of this truth is golden.

As I noted elsewhere, a group of European Central Bank economists have just said the quiet part out loud.

In a recent report, they warned that rising demand for physical gold (over 2000 tons from London to NYC in 2025) could send the European Union into collapse.

Why?

Because the Eurozone, already teetering on skyrocketing debts and rising bond yields (and hence interest rates), doesn’t have the money nor the gold to meet their 100:1 levered gold derivative contracts hitherto floating on the London and NY Gold Exchanges with a gross exposure of over $1T.

Yes, One TRILLION.

Sadly, we’ve been warning of this derivative time bomb and Comex insanity for years, yet only now the ECB is confessing its trillion-dollar problem out loud.

These metals exchanges, which rolled over and extended paper gold contracts since the 1970s to artificially short (i.e., price control) the gold price, were basically credit exchanges, not gold storage providers…

But now they are seeing counterparties wanting the physical gold itself rather than just their extended paper contracts.

Unfortunately, the Eurozone doesn’t have the gold their contracts promised.

In short, they are caught in a lie.

The other lie is trying to “blame” this leverage trap on gold while failing to confess that counterparties are seeking actual gold delivery to cover their own past sins.

That is, they need the gold because they trust this hitherto “pet rock” analog asset as a far, far superior store of value and reserve asset than the sovereign bonds and paper currencies they’ve been destroying for decades—something we have also been forewarning for years.

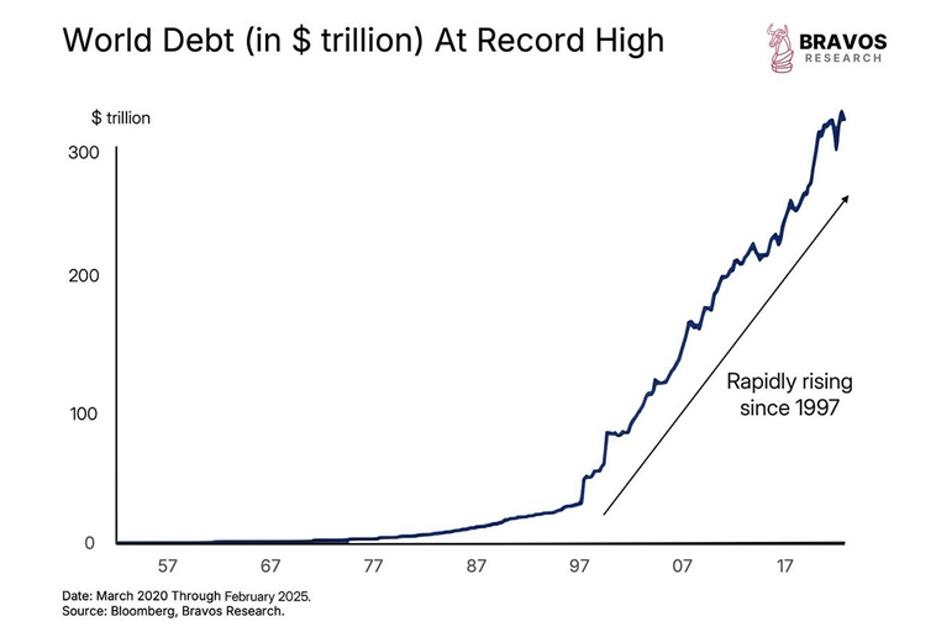

In other words, gold is no longer just a hedge or matter of speculation, it’s THE emerging global Tier-1 asset which even those folks at the BIS and IMF (notorious for “bending” truths) now openly recognize as THE reserve asset in a world openly losing confidence in the debased paper money and distrusted IOUs from a world falling off a $300T global debt cliff.

In short: Gold is calling BS on an entire global financial system whose dishonest fantasy policies of thinking they could take sovereign debt levels to unprecedented/historical and drunken levels to buy time, votes and wealth inequality without a hangover.

Or stated more simply, gold is unmasking the lie of deficits without tears, money printing without currency debasement and debt without destruction.

When I think of such “leaders” and financial policies, I am again reminded of Mark Twain, who observed: “I sometimes wonder if the world is being run by smart people who are putting us on, or by imbeciles who really mean it.”

No Surprise at All

But such imbecility (or dishonesty) is no surprise to those who understand math, history and sound money—i.e. those who understand gold.

For years, family offices, private wealth advisors at lofty bank X, Y&Z and even RIA A, B&C have been telling themselves (and you) that gold is just too “volatile.”

Gold has been less than a 1% allocation for most family offices and an even lesser allocation for all other investors for years and years.

But gold has outperformed the S&P (at even a total return basis) for TWENTY years, and is the highest performing asset of 2025.

Under NO stretch of the imagination (or even objective math) is this asset even close to being “too volatile” of late.

Far more importantly, gold’s real secular move has yet to even begin, despite over two (largely ignored) decades of outperforming traditional risk assets.

Meanwhile, the so-called “smart money” – from the Harvard Endowment to Family Office A, B&C–are stuck in private credit pools (what Jeffrey Gundlach described as the new “weapons of mass destruction”) and other non-marked-to-market PE timebombs whose hey days are about to become dark days in the illiquidity that defines all credit cycle implosions, toward which we are marching at top speed.

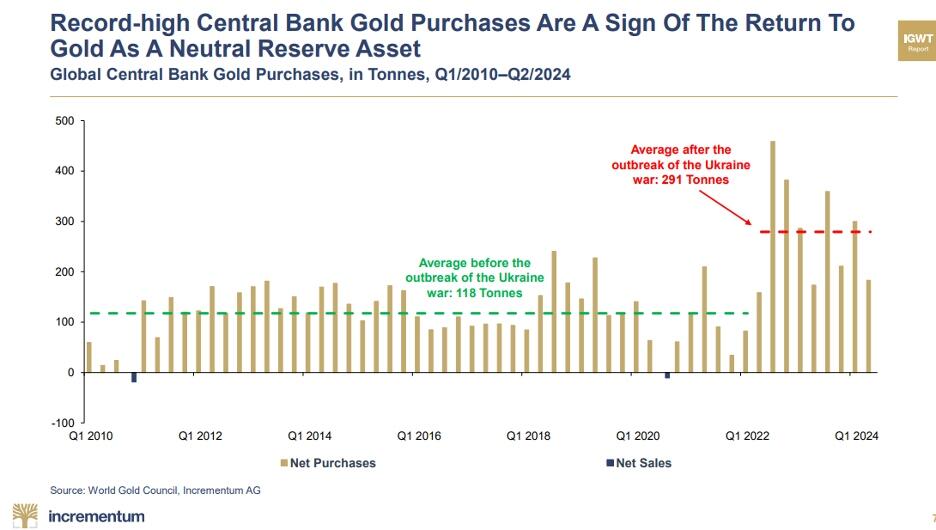

And in this very strange backdrop, the very central bankers who have downplayed, ignored, and intentionally misrepresented gold, are now buying it at record levels.

In short, even the liars are now stacking the hidden truth.

The ironies. They do abound.

Two Storms, One Harvest

Every food crisis in living memory has been a one-shock event. The 2008 price spike was a commodity bubble. The 2020 shortages were a logistics failure. The 2022 grain scare was a war on one exporter’s ports. Each time, the system bent, adjusted, and recovered, and each time the experts assured us afterward that global markets are simply too big and too diversified to fail.

What nobody in Washington seems eager to discuss is that 2026 is shaping up to be something the modern food system has never actually faced. Two independent shocks, one climatic and one geopolitical, are converging on the same harvest cycle at the same time. Not sequentially. Simultaneously.

Start with the weather. The Pacific Ocean is currently building toward what forecasters now openly call a record event. NOAA’s Climate Prediction Center puts the odds of at least a strong El Niño near 88 percent, with roughly two in three odds it reaches “very strong” status, the tier reserved for perhaps three or four events in the entire satellite era. Every major global model now projects a median peak in Super El Niño territory, and most of them project it exceeding the 2015-16 event, which until now held the modern record. Sea surface anomalies were already brushing the super threshold in mid-July, months before these events normally peak. The atmosphere has already shifted into El Niño mode, and the event is forecast to crest in late fall and early winter.

This is not about “climate change.” It’s about the standard cycles of weather, and the cycle we’re currently in is one that has likely devastated societies in the past. We’re better prepared as a society today, but not all Americans are equally prepared.

Serious households have started doing the quiet math on their own. Grocery bills tell part of the story, and the forecast maps tell the rest, which is why long-term food storage has moved from fringe hobby to mainstream line item in the family budget, with established suppliers like Heaven’s Harvest seeing demand from people who five years ago would have rolled their eyes at the idea. That instinct is not paranoia. It is pattern recognition, and the pattern is worth walking through carefully.

Editor’s Note: Heaven’s Harvest IS a sponsor, but the warnings of this article are real and would be written even if we didn’t have a survival food sponsor. With that said, those who take advantage of what they offer can use promo code “Patriot” for 15% off.

The Fertilizer Clock Is Already Running

While the Pacific warms, the second shock has been unfolding in the Strait of Hormuz. The conflict with Iran turned the world’s most important energy chokepoint into a contested waterway, and the consequences reach far beyond the gas pump. Roughly a third of global fertilizer trade moves through Hormuz, and the disruption sent urea prices up 86 percent year over year by March, with a 53 percent jump in a single month.

The World Bank projects energy prices rising about 24 percent in 2026 and fertilizer about 31 percent. By its own accounting, fertilizer prices ran 35 percent higher in the first five months of this year than the same period last year.

Here is the mechanism the nightly news will not explain. Fertilizer is not a grocery item. It is a time-delayed input. The nitrogen a farmer in Iowa or Punjab could not afford to apply this spring does not show up as a problem this spring. It shows up as a thinner harvest six to twelve months later.

The World Bank’s own food security brief concedes that the effects of reduced applications earlier this season “are likely to become visible only later in harvest outcomes.” Translate that from institutional language into plain English and it means this. The damage is already done, it is already in the ground, and we are simply waiting for it to arrive on the shelf.

Now check the calendar. Six to twelve months from the spring planting season lands us squarely in late 2026 and early 2027. Which is precisely when the strongest El Niño in the instrumental record is forecast to peak, bringing its signature droughts to Southeast Asia, Australia, southern Africa, northern Brazil, and South Asia, the very regions that grow the world’s rice, sugar, and oilseeds.

The World Bank warns openly that a strong El Niño “could disrupt multiple crop belts simultaneously” on top of the conflict-driven input costs. Their baseline projection assumes the Middle East disruptions ease by autumn. What in the last two years of Middle East history suggests that assumption is safe?

The System Has No Slack Left

The comfortable answer is that global markets always adjust. But adjustment requires slack, and the slack is gone. Global cereal production is expected to decline from last year’s records even before El Niño does its work. The UN World Food Programme, hardly a den of right-wing preppers, is calling this the most significant disruption to its supply chains since Covid and the invasion of Ukraine, and its supply chain director put the stakes bluntly.

Today’s supply chain challenges are tomorrow’s hunger crisis.

There is also a political dimension that markets cannot price. When food gets scarce, governments do not behave like economists. They behave like politicians. Export bans, hoarding mandates, and panic buying at the national level turned the modest rice shortfall of 2008 into a global crisis, and analysts are already warning that import-dependent nations are the first dominoes.

The 2015-16 Super El Niño, a far weaker event than what is now forecast, threw tens of millions into food stress across Africa and Asia. This one is projected to be stronger, and it arrives with fertilizer already rationed by price and shipping lanes already contested by missiles.

What Joseph Knew

Scripture does not treat preparation for lean years as faithlessness. It treats it as wisdom delivered in advance to those willing to act on it.

Behold, there come seven years of great plenty throughout all the land of Egypt: And there shall arise after them seven years of famine; and all the plenty shall be forgotten in the land of Egypt.

Joseph did not respond to that warning with a hashtag or a committee. He stored grain during the years of abundance, and when the famine came, Egypt stood while its neighbors begged. The lesson is not that famine is certain. It is that the time to prepare is precisely when preparation still looks optional.

Nobody who filled a pantry in a year of plenty has ever regretted it, and nobody standing in an empty aisle has ever been glad he waited for certainty.

None of this calls for panic, and panic is the enemy of sound judgment anyway. It calls for the same unglamorous prudence our grandparents considered ordinary. Keep some cash margin, know your local growers, and put real food in deep storage while it is cheap and available, because the entire arc of this story is that cheap and available is a closing window.

Families looking for a straightforward place to start can visit Heaven’s Harvest and use promo code Patriot for 15 percent off long-term storable food. The forecasts may yet soften, the strait may yet reopen, and we should pray they do. But hope is a fine thing to hold and a foolish thing to eat.

{kind=link}